tl;dr

- This year, I’ll allocate my money to: keeping a ~$15,000 float in my checking account for outstanding expenses, $23,000 (+ $11,500 employer match) in a Traditional 401k, $34,500 in a “Mega Backdoor Roth 401k”, $7,000 in a Backdoor Roth IRA, $750 in a Flexible Spending Account (FSA), and the rest into my regular old investment account.

- The accounts I’ll be avoiding putting money into are: an Emergency Fund (here’s why), a Commuter Benefits Account (my employer already gives me more than I can use), Health Savings Account (HSA) (I don’t like the incentive it creates for me to not get healthcare), Dependent Accounts like 529 College Savings Plans and Dependent Care FSAs (I don’t have dependents), Whole Life Insurance (it’s almost universally a bad investment).

Intro

This post is about the accounts I’ll be putting my money into this year, but is also meant to provide a guide to others. It’s based on what I think is optimal for my own situation and –as always– the more similar to me you are to me, the more applicable it will be to you.

Where My Money Will Go

This year, I have / will continue to allocate my money to the following accounts, in roughly this priority order:

- ~$15,000 – Checking Account: My first priority is always making sure I always have enough money in cash to cover my outstanding credit card bills and anticipated upcoming expenses (eg. mortgage payments and estimated tax payments). This usually means I keep ~$15,000 in my checking account1.

- $23,000 + $11,500 employer match – Traditional 401k: Once I have enough float in my checking account, I put every penny into my Traditional 401k. Whether it makes sense to prioritize a Traditional or Roth 401k topic beyond the scope of this post (and is covered well here), but regardless of which one I chose, I’d still prioritize filling it up before all the accounts later in this list. My rationale is that my employer match makes this account higher leverage than any of the others. With this account, putting in $23k lets me actually invest $34.5k in the market. Given that the market goes up on average over the decades-long time horizons I’m looking at, getting this leveraged investment into the market earlier will result in more returns.

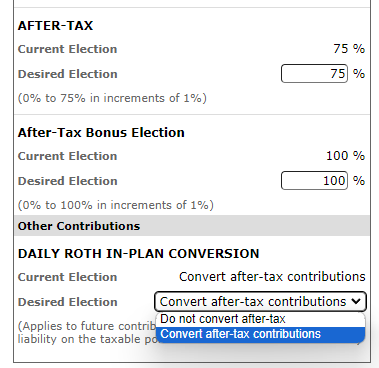

- $34,500 – “Mega Backdoor Roth 401k”: My next investment priority is the Mega Backdoor Roth 401k. I touched on this trick in the article about optimizing finances when changing employers. The gist of this trick is that you are contributing money to your 401k plan after tax (ie. with zero tax advantages compared to just a regular investment account), and then you convert that after-tax money into a Roth 401k via an “in-plan conversion”. The end result is that after I’ve deducted my $23k elective deferral and $11.5k employer match from my plan’s overall contribution limit ($69,000 in 2024), I’m able to use the rest of the space in the plan as Roth 401k space.

This trick sounds complicated and potentially sketchy, but it really isn’t. My 401k provider (Fidelity) literally has an article about it on their website and provides a simple dropdown box to enable the backdoor automatically on contribution: - $7,000 – “Backdoor Roth IRA”: The Backdoor Roth is similar to the Mega Backdoor Roth described above, but is done with an IRA, rather than an employer sponsored 401k Plan. I do the Backdoor Roth, instead of a regular Traditional or Roth IRA contribution, because each of those accounts have income limits above which you’re not allowed to contribute directly ($87k and $161k, respectively). Similar to the Mega Backdoor, this technique is legal (despite the sketchy name) and is even blessed by the IRA. Performing the backdoor is as simple as 1) having an IRA and Roth IRA account, 2) contributing the money to the IRA account, and then 3) transferring the money to the Roth IRA account. It only takes a few minutes, and you can find instructions online for any major brokerage (eg. here’s some for Schwab).

Note that it’s easy to make a mistake when entering the Backdoor Roth on your taxes, so watch out for that (and warn your accountant that you did this, if you use one). Also note that if you have a Traditional IRA (eg. if you used my trick of rolling over a 401k to an IRA to get relationship pricing or a bonus), you’ll need to make sure you don’t fall afoul of the pro-rata rule. - $750 – Flexible Spending Account (FSA): My $750 FSA contribution is deducted bit-by-bit from every single paycheck. I use it for co-pays, prescriptions, and over-the-counter costs like sunblock. Even though it is a tax-advantaged account, I explicitly don’t max out this account to its $3,200 limit (for 2024). I limit my contributions because it’s a use-it-or-lose-it type account where you can only rollover $640 (for 2024) each year, and the remaining money in the account is lost. Historically, I haven’t had enough medical expenses to need the full $3,200, so I don’t want to risk contributing that much as losing it.

- $The Rest – Investment Account: Any money left after I use all my tax advantaged accounts (and pay my bills) goes straight into a boring old investment account. I have a specific asset allocation I prefer based on the Boggleheads Three Fund Portfolio, and I use the new money to rebalance my account by buying the ETFs that are under-represented relative to my chosen allocation.

Where My Money Won’t Go

There are plenty of other types of accounts that offer tax advantages or other benefits, which you might have heard recommended at some point. I intentionally don’t contribute to any of the accounts on the below list. That doesn’t necessarily mean they’re bad (in fact I know people that could benefit from most of them), but they’re not right for me:

- Emergency Fund: This one already got a whole article to itself. The short version, however, is that I think I have enough savings and access to credit to weather the kind of events emergency funds are designed for (unexpected expenses, job loss, etc.).

- Commuter Benefits Account: I actually do have a commuter benefit account. My employer puts $260 / month into it on my behalf. I could put another $55 in each month to bring it up to the $315 limit (for 2024), but I don’t have enough commuter expenses to use up that extra contribution. This account isn’t annually use-it-or-lose-it like FSAs are, but you do lose it when you leave your employer (which is why I recommend draining it when changing jobs). For me, it doesn’t make sense to bank any extra money in an account that will probably go away before I can ever use it.

- Health Savings Account (HSA): Health Savings Accounts are often hyped as a “triple-tax free” account. When viewed solely as an investment vehicle, they are pretty amazing; they basically combine the advantages of a Traditional and Roth account. The problem, for me, is that you need to be on a High Deductible Health Plan (HDHP) (which, as the name implies, is a plan with higher initial costs to access healthcare) to be eligible for them. My employer offers one of these plans, and even makes a contribution to your HSA to cover the increased costs of the plan.

The problem with having an HSA + HDHP is it creates an incentive to delay or avoid seeking out health care. Yes, my employer’s contributions to my HSA would cover my deductible if I go to the doctor, but I get to keep those contributions whether or not I go to the doctor. So I make money by not going to the doctor, and lose money by going. I know myself, and I don’t want that kind of financial incentive to avoid getting the care I may need. - Dependent Accounts: There are plenty of tax advantaged accounts aimed at helping people take care of their dependents, such as 529 College Savings Plans and Dependent Care FSAs. I don’t have children or other dependents, so I have no use for these accounts.

- Whole Life Insurance: Whole life insurance is sometimes pitched as an investment vehicle. While it does have some niche tax advantages, it’s almost universally a bad investment.

- This isn’t actually a checking account, but it acts like one. It’s a Fidelity Investment Account that I use as a sort of checking account. It auto-invests in Money Market funds, allowing me to earn rates comparable to the best current promotional savings rates, without having to chase those rates across banks. ↩︎

Leave a comment