tl;dr

- This article summarizes all the tax mistakes my friends and I have made, and how to avoid them.

- Tax time mistakes:

- Import Errors: TurboTax can screw up importing W2s that have multiple states on them. Never trust automated imports; re-check everything.

- RSU Cost Basis Error: Depending on how you punch in RSU sales, you may be required to mail in a physical copy of your 1099-B after e-filing. If you fail to do so, the IRS may try to double tax your RSUs.

- Backdoor Roth Entry: Backdoor Roth conversions are easy to punch into TurboTax wrong. Follow these instructions when punching them in, and always keep an eye on TurboTax’s running total at the top of the screen for taxes owed. You can catch many mistakes by checking how that total changed vs how you expected it to change.

- Year round mistakes:

- RSU Underwithholding: RSUs are chronically under withheld at 22%. Adjust your withholdings, or pay estimated taxes throughout the year, to avoid a tax season penalty.

- PFICs: Foreign mutual funds and ETFs may be considered Passive Foreign Investment Corporations (PFICs), which have disadvantageous tax treatment. Avoid owning them, own them in an exempt account, or be ready to hire someone to deal with the reporting pain.

Intro

With tax season in full swing, I just watched my coworker get burned by a TurboTax bug that made him think he owed tens of thousands of dollars. There are plenty of tax mistakes one can make, and both my friends and I have made mistakes that made it into the five figure range (before being corrected). This article attempts to summarize the causes of all those mistakes, and the best ways I’ve found to avoid them.

Filing Mistakes

W2 Import Errors ($10k+ example)

If you are taxed in more than one state, you’ll get a W2 showing income and taxes paid for each state. For example, as a Tech worker based in New York, but doing business travel to California periodically, I end up meeting the threshold to pay California income tax. The problem with this is that TurboTax has had a bug for years that means it only imports one state W2, and drops the rest (at least for my company’s payroll provider). The result of this is that TurboTax will calculate your state taxes as if you hadn’t paid anything yet, resulting in it showing a massive amount owed. This resulted in a five figure tax surprise for my coworker, who ended up having to pay an accountant hundreds of dollars to solve the mystery for him.

Avoiding This Mistake

This is sadly one of many TurboTax import errors I’ve had myself, or heard from others. The key lesson here is:

Never trust TurboTax’s auto-import features. Always double check them against your copies of your forms, or just punch them in manually.

Miss-reporting RSU Cost Basis ($10k+ example)

Context

When I receive Restricted Stock Units (RSUs) from my employer, they are taxed as income when they vest (i.e.. when they show up in my brokerage account). My company sells RSUs on my behalf to cover the taxes, sends that money to the government, and at the end of the year gives me a W2. That W2 counts my RSUs as income and shows the taxes my company remitted on my behalf. The price my RSUs vested at then becomes my cost basis for those stocks. When I sell my RSUs, I only owe taxes on the difference between the vest price (cost basis) and the sale price (proceeds).

Concretely, if I vest $10,000 in stock and sell it for $11,000, I will have paid income tax on the $10,000, and that will be reflected in my W2. I will then owe capital gains tax on the $1,000 of gains. The capital gains tax must be calculated and given to the government during tax season1.

If you receive RSUs and choose to sell them2, you should receive a 1099-B tax form from your brokerage. That form outlines, among other things, the cost basis and the proceeds for the sale. This is an excerpt from the form I received this year:

Notice the highlighted “basis is available and not reported to the IRS”? That’s important. That means that the IRS won’t know you already paid income tax on these RSUs, unless you tell them. The way you tell the IRS about this basis is by filing your taxes, but that comes with some gotchas.

The Mistake

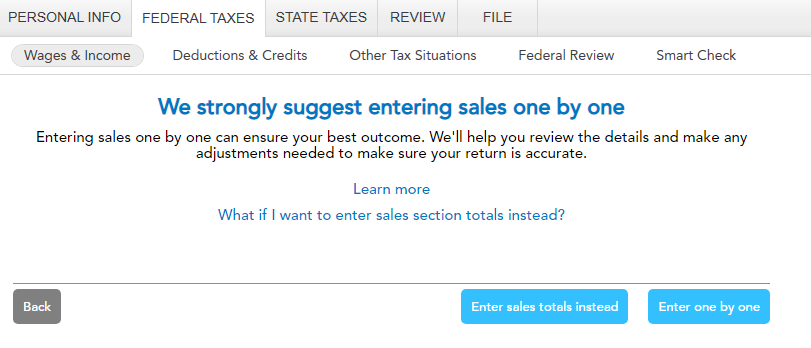

If you manually punch in your 1099-B form into TurboTax 2024 Desktop, you’ll be faced with a screen like this:

If you had many transactions in your account, it may be easier to select the “Enter sales totals instead” option, rather than punching in dozens of transactions. If you choose to use TurboTax’s auto import feature (bad idea; see the previous section), it appears that it will also produce the same result as it would have if you manually punched in only the sales totals.

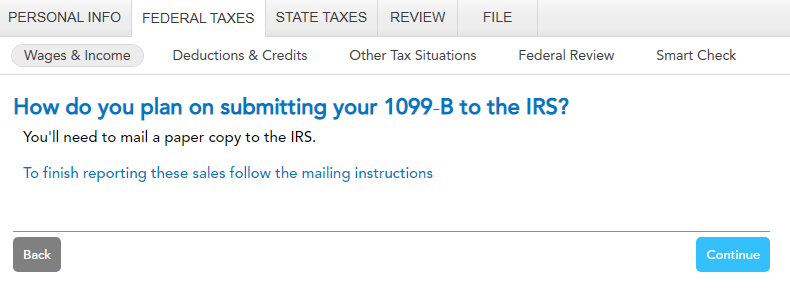

In either situation, you should see this screen afterwards:

What this means is that after you e-file your tax return, you will also have to mail a physical copy of your 1099-B (along with a Form 8453 that TurboTax will generate for you) to the IRS (note that if you use TurboTax Online instead, you can allegedly upload a digital version of this form instead). If you forget to do this, the IRS will re-evaluate your taxes assuming you had a $0 cost basis in your RSUs. That reevaluation will result in double taxation of your RSUs, and a CP2000 Notice telling you to pay up. A friend of mine made this mistake, and got a five figure tax bill. He almost paid it, until I pointed out this common mistake to him.

Avoiding This Mistake

In short, this mistake happens when:

- You have a 1099-B that says “basis is available and not reported to the IRS”

- You auto-import your RSU sales

OR

You elect to manually punch in totals, and not every individual transaction, when entering the 1099-B into TurboTax - You forget to mail a physical copy of your 1099-B to the IRS after e-filing

Avoiding any one of those steps should prevent this from happening to you.

Incorrectly Entering Backdoor Roth (~$3k example)

I, and many of my peers, contribute to Backdoor Roth and Mega Backdoor Roth accounts. The core component of both tricks is putting post-tax money into an account that normally holds pre-tax money (either IRA or 401k), and then moving that money into the equivalent Roth account. Taking money out of a pre-tax account is normally a taxable operation, but in the case of these backdoor techniques, it is not taxable. The problem is that it’s very easy to accidentally punch your forms into TurboTax in a way that makes it think you owe taxes. If you do this, TurboTax will calculate that you owe full income tax on the withdrawn amount, which will likely end up in the ~$3,000 range (plus possibly penalties).

Avoiding This Mistake

To avoid making this mistake, follow these instructions.

My general strategy to avoid mistakes like this when punching anything into TurboTax is:

- Know whether I expect it to make my taxes go up, down, or stay the same.

- Note down the running Federal and State refund amounts at the top of the screen, before punching anything in.

- Punch in my forms.

- Check that the amounts owed moved in the directions I expected (eg. in the case of Backdoor Roths, the amount should be unchanged).

Year-round Mistakes

Underwithholding RSUs (~$1,300 example)

As I mentioned above, RSUs are taxed as income. A caveat, however, is that your company is only required to withhold federal income tax from them at a rate of 22% (until you reach $1,000,000). Most people in this blog’s target audience probably owe more than 22% income tax at the end of the year, meaning that if you get RSUs the income tax for them will be underwithheld. You will owe a penalty if you paid less than than 90% of what you owe this year, or 110% of what you owed last year3. For 2024, the penalty is set at an 8% interest rate, which can add up.

For example, let’s assume you vested $200,000 in RSUs at $50,000 quarterly, and had a 35% federal marginal tax rate. The default 22% withholding rate would be 13 percentage points short of what you owe, meaning you’d underpay $50,000 * 0.13 = $6,500 each quarter. At this year’s 8% rate, that would work out to $1,300 in penalties.

Avoiding This Mistake

You can avoid4 these penalties in a few ways:

- Increasing the taxes your employer withholds: My employer now lets us adjust our withholdings rate on RSUs upwards. Before that was supported, another option was asking for extra withholdings from our salary, and attempting to get it to roughly balance out the taxes on the RSUs.

- Paying estimated taxes: I prefer to make quarterly estimated tax payments directly to the IRS. I put the payment on credit cards, to make money off the sign up bonuses.

Holding Foreign Mutual Funds and ETFs

When I left Canada, I thought I would be clever by stashing all my money in a TFSA (Canadian equivalent to a Roth IRA). I knew that the US wouldn’t recognize its tax advantaged status, but my plan was to just leave the stocks in there and never touch them. I figured if I didn’t sell anything, there would be no taxable gains for the US to come after, and I could access them when I eventually returned to Canada.

The problem is that Canadian ETFs and Mutual funds (as well as many similar products in many other countries) are considered Passive Foreign Investment Corporations (PFICs). PFICs are a massive and complicated topic, but suffice it to say that they can lead to very unfavorable tax treatments. In my case, I ended up having to take the mark to market election on the ETFs I owned. This treatment means I was taxed on the ETF’s gains as if they were income, even if I didn’t sell any shares. Even worse, I had to fill out a 4-page form, per ETF I owned shares in. These forms aren’t supported by TurboTax, and tax preparers charge an arm and a leg to do them. In the end, I (un)luckily had losses on these ETFs and thus didn’t end up owing any additional taxes, but the process was miserable. I ended up selling all my Canadian ETFs to avoid the painful process and negative tax treatments.

Avoiding This Mistake

I see a few ways to avoid the problem of PFICs:

- Just don’t own PFICs (ie. foreign mutual funds, ETFs, etc.).

- Only hold PFICs in exempt accounts (eg. Canadian RRSP accounts are exempt from PFIC reporting requirements).

- Get enough of a benefit from holding PFICs that it’s worth paying the tax penalties and the cost of an accountant to deal with this mess for you.

Contacting the IRS When Something’s Gone Wrong

Surprisingly, you can just call and talk to someone at the IRS. In my own personal experience, and through anecdotes from friends, IRS agents are pretty knowledgeable and helpful. Around tax season, their lines are incredibly backed up and impossible to get through. An alternative is calling the Taxpayer Assistance Center line (open the “Your local IRS office” section) to get an appointment for help. Anecdotally, if your problem is simple enough, the agents on the reservation line will just resolve the issue for you.

- Or earlier, if you choose to pay estimated taxes. You might choose to do that, for example, to avoid underpayment penalties. ↩︎

- I absolutely think you should; but that’s a topic for another post. In the mean time, this topic has already been covered well on FAANG FIRE, a blog I quite enjoy and follow. ↩︎

- You may have heard 100%, rather than 110%, thrown around as the percentage of last year’s taxes you need to pay to avoid a penalty. 100% is the default number, but once you have an adjusted gross income (AGI) over $150,000, the threshold goes up to 110% ↩︎

- In previous years, this rate used to be as low as 3%. At that rate, it made sense to some people to just pay the penalty, rather than go out of their way to fix the underwithholding during the year. At a 3% rate, it could be reasonable to expect a higher return from investing that money in the meantime before using it to pay your taxes. ↩︎

Leave a comment